The money Nepali workers send home from abroad has been propping up the country’s economy, but there are fears the global economic slowdown caused by the COVID-19 pandemic will lead to a drastic reduction in remittances.

While Nepali workers overseas find their earnings shrink because of quarantines or shutdowns, back home their families find it difficult to go to remittance companies to collect cash to buy essentials due to the lockdown.

“I used to send money back home every month. I received my payment last week and transferred the amount using my mobile banking app, but my family has not been able to receive the amount back home because of the restrictions,” Krishna, a worried migrant worker told us on the phone from Qatar. “The work we are doing is for our families. What is the point of working during such risky times if our families continue to struggle?”

Krishna’s wife Laxmi lives in Tanahu with her in-laws and two small children, who are all dependent on the money Krishna sends home. “The cooperative through which I used to get money from my husband is closed. The other bank branch is a 30-minute walk and there is a lockdown,” said Laxmi, who family borrowed from friends to send Krishna overseas, and they are asking for their money back because they are also going through difficult times.

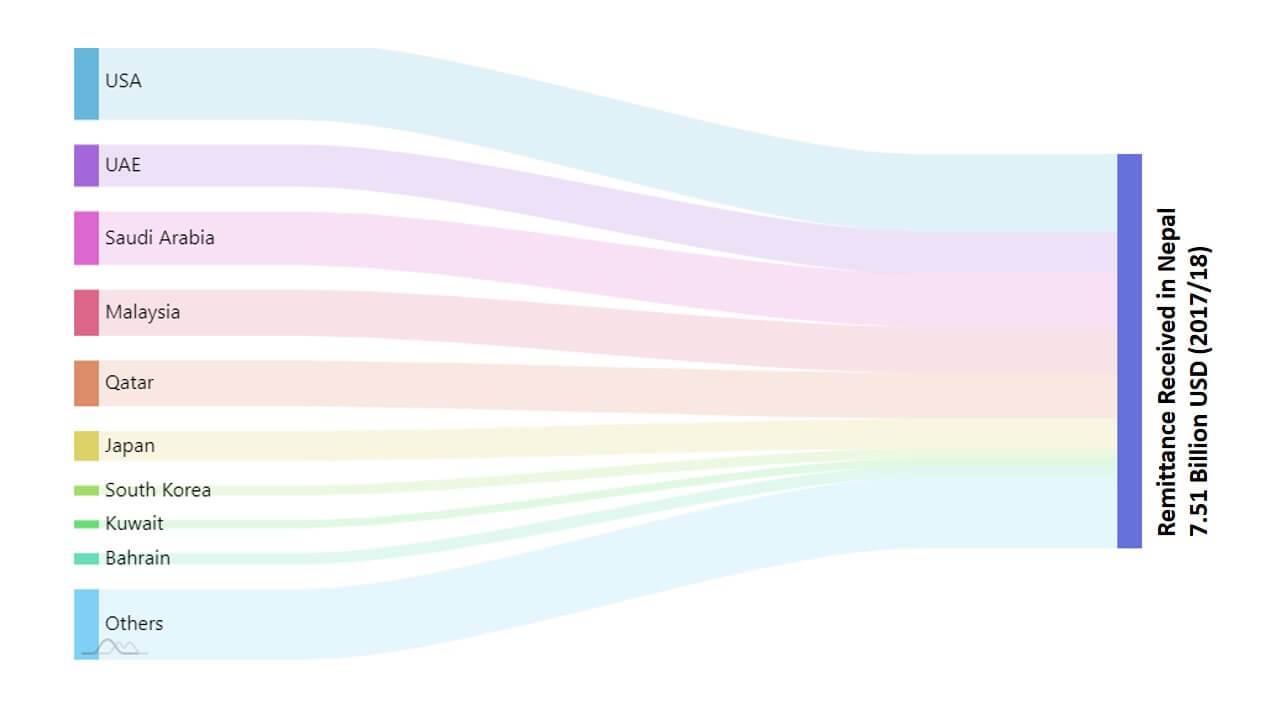

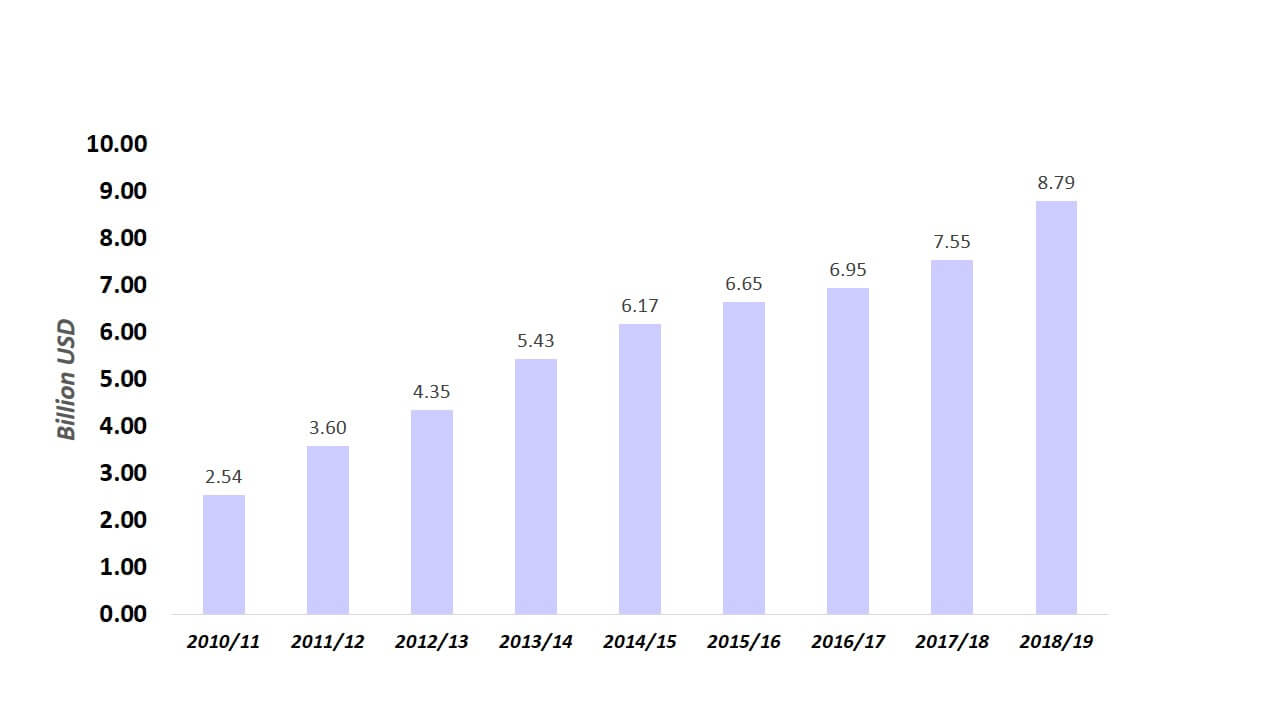

Nepalis working in the Gulf, Malaysia, Korea and Japan and other countries sent home $8.75 billion in 2018/19 through official channels, and Nepal is among the top five countries in terms of remittance-to-GDP equivalence which has consistently remained above 25%.

Remittance has been increasing steadily in the last decade. However, even before the pandemic there were concerns about the future of remittances as the volume of labour migration has been falling since 2014. The coronavirus crisis has further heightened these concerns.

Nepal Rastra Bank’s Gunakar Bhatta acknowledges that the extraordinary measures need to be taken to deal with the unprecedented crisis which has affected the financial sector. The Central Bank has issued a circular asking remittance companies to continue their services, and some have been given passes to travel to work.

“We have requested banks to provide minimum services at least for a few hours a day while also taking high precautionary measures to ensure that customers and staff are safe,” Bhatta said.

Remittance companies and the private sector have tried to adapt to the crisis. Branches are providing service for limited hours a few times a week on a rotational basis. Their websites list contact information of bank representatives, with hotline services.

Diwakar Thapa, former president of the Nepal Remittance Association, acknowledges there are practical challenges for the smooth operation of this agent-based model during the crisis, especially outside the capital. The proliferation of thousands of money transfer agents across the country had helped migrant families to receive money through formal channels.

But after the lockdown, most agents are closed, and only a few have figured out ways to operate from their homes or to coordinate with the local governments to allow operations for limited hours.

“Our normal services are disrupted, but if enough customers call us, we adjust our hours or days of operation,” says a Bhairawa-based bank representative.

Another worker in Qatar said he was told not to report for duty, but was getting basic pay. He says the disruption in money transfer mainly affects new arrivals whose families depend solely on remittances, or they have to pay back loans to recruiters.

“I can get away without sending money for a month or two but there are others for whom this is costly,” he added. Many others are not comfortable using mobiles for transfers.

A Nepali who works in a hotel in the UAE said he was holding on to his March salary. “Things are so uncertain here, who knows, I may need that the money to buy my ticket back home, my family is managing,” he said.

Some Nepalis have moved to digital banking after fees were waived, transaction limits raised and remittances could be directly transferred to digital wallets. But with low internet penetration rate, and many still unfamiliar with online and mobile payments, there are not many using this route.

Says Bhatta of Nepal Rastra Bank: “Remittance is an important source of income for both families and the economy. It is a priority to adopt measures to maximise incoming flows, we have to try to accommodate individual emergency cases.”

He said when clients have pressing needs, financial institutions can coordinate with the District Administration Office to get passes during the lockdown.