It is noon at the nerve centre of Daraz Nepal in Naxal, and the place is humming like a bee hive. Orders are constantly coming in online, and going out for delivery. No one has time to talk.

Across town at eSewaPasal in Kupondole, the scene is relatively more relaxed, but only because it is already 2PM and most of the day’s online orders have already been shipped.

Daraz Nepal and eSewePasal are two of the swarm of new e-commerce companies that are poised to turn Nepal’s retail market upside down. After Alibaba acquired the Pakistani online site Daraz and BhatBhateniOnline merged with Nepal’s leading mobile-wallet company eSewa, an e-commerce wave is sweeping urban Nepal.

“Compared to our past operation as BhatBhateniOnline, we now have exponential growth within just half a month of functioning as eSewaPasal,” explains CEO Manish Shrestha. “We are therefore expanding our inventory from 15,000 to 60,000 items by December.”

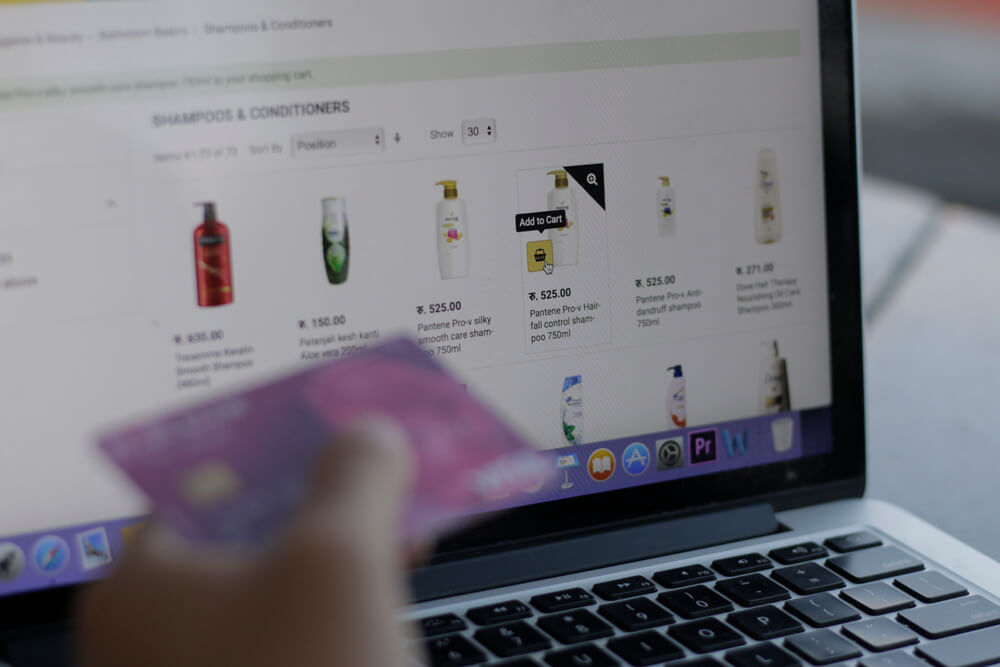

eSewaPasal has made online payment accessible with options for credit/debit/prepaid cards, eSewa and PayPal for international payment. Customer confidence in digital payment got a boost after Nepal Rasta Bank licensed online payment companies -- eSewa, IME Digital Solution and Prabhu Technology -- and allowed 28 banks mobile and internet banking.

Currently, there are 1 million eSewa customers and nearly 5 million mobile banking clients all over the country, and these numbers are expected to rise with increasing mobile internet use, and the proliferation of smartphones.

“E-commerce, like any other business, is driven by its ecosystem. At the moment, the growth is just organic, and to increase the pace we need greater awareness and trust in internet payment,” explains Roshan Lamichhane of eSewa, taking the experience of Amazon India which uses mass media, and not just social networking sites, to create great first impressions and to advertise their deals and offers to attract customers.

“Here too, businesses should also advertise on how to navigate through the online sites so that people do not get lost in the maze of products,” Lamichhane adds.

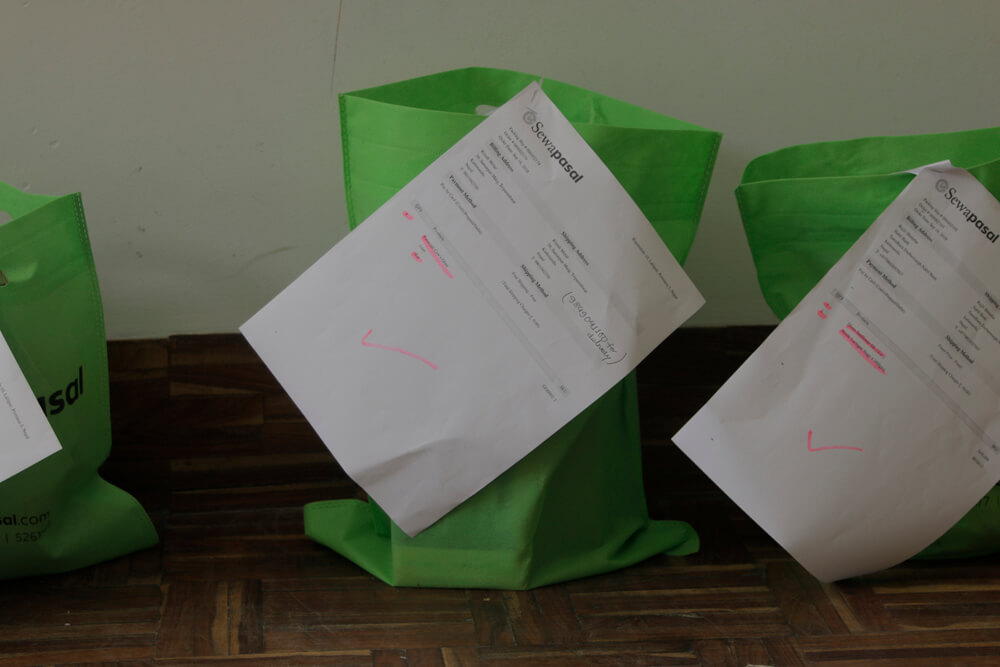

Most online sites today rely on cash payment on delivery, but it is limited by poor infrastructure and lack of street addresses. The delivery person rides through traffic on a scooter and has to call numerous times for directions before finally finding the house.

Online payment by credit or debit card would streamline e-commerce, but it has never really taken off in Nepal. Digital shopping still being a niche market limited to main cities, banks are not yet excited about extending their services.

International online purchase by credit card is also hindered by Nepal Rastra Bank’s regulations on cross border payments because of money laundering concerns, and the danger of credit card fraud. Another obstacle is the requirement by international card companies like Visa for Nepali banks to have a large asset base as collateral, as well as the absence of an online payment culture.

“For most customers, e-banking is mainly necessary for paying utility bills, top-up and recharge and that does not require credit cards,” says Ritesh Lamichhane of Bank of Kathmandu.

Banks introduce credit cards, but it is loss-making because of the low rate of e-banking. Says Govinda Gurung of Civil Bank: “It is like a gold necklace, you buy it at huge expense but can only show it off on special occasions.”

Read also: Kathmandu’s Silicon Alley and the Law, Sonia Awale

Working at home, Sahina Shrestha

The vacuum left by credit card payment is filled by online payment through mobile phones. Companies are working to use Nepal’s growing mobile penetration rate to push safe transactions through mobiles with two-factor authentication. Again, there is no universal mobile payment system through a consortium of banks yet, and most online shopping sites have their own payment app.

Still, the exponential growth in companies like the motorcycle ride-sharing company Tootle shows that there is a huge pent-up demand and a wide variety of trading activities that could switch to online.

E-commerce businesses are not waiting for the banking sector to improve digital transactions – they are already busy delivering orders in and outside Kathmandu. Daraz Nepal, for instance, is busy adapting Alibaba’s tools to facilitate online shopping in Nepal.

It wants to increase customer engagement with more than 80,000 products by getting brick-and-mortar merchants and retailers to sell online.

Says Daniel Shrestha of IME Pay: “There has to be broader collaboration among the service providers. Our competition is not with each other, but with cash.”

Read also: Focus on agriculture and tourism, Sikuma Rai